When it comes to growing your wealth, one concept stands above the rest: compound interest. Whether you’re investing in stocks, bonds, mutual funds, or even saving for retirement, compound interest helps your money grow faster than simple interest. But what is it, exactly? How does it work, and why it can be a powerful tool for investors?

In this blog, we’ll break it all down for you with examples and step-by-step calculations. So, let’s dive in.

The compound interest is interest accumulated on your initial deposit or loan along with its accrued interest or interest earned on interest.

Compounding schedules can range from a daily to an annual basis, but the time frame when the interest is actually credited or debited to/from the account can be different.

A compounding period is the amount of time between when interest compounds (at discrete intervals) or is credited to your account.

The higher the compounding period, the more your money grows.

What is compound interest?

Compound interest is often described as “interest on interest.” It’s the process where the interest you earn on an investment is added to the principal (the original amount invested). This means that the interest you earn over time starts to earn its own interest, creating a snowball effect that helps your wealth grow exponentially.

The key difference between simple and compound interest is that simple interest is calculated only on the initial principal. Compound interest, however, takes the interest already earned and applies it to the principal to calculate additional interest. Over time, this leads to a much higher return on investment (ROI).

To make it clear, let’s consider this example:

If you invest $5,000 in 2026 at a 7% annual return:

With simple interest, you’d earn $350 annually, totaling $8,500 after 10 years.

With compound interest, your money grows on itself, reaching about $9,836 in the same period.

The difference may not seem huge initially, but over decades, it can result in significantly greater growth. This is why compound interest is a cornerstone of investing – it rewards time and patience, helping your money grow faster the longer it is invested.

How does compound interest work?

To understand how compound interest works, it’s important to know that it depends on several factors:

Principal amount: The original sum of money amount of money you invest or deposit.

Interest rate: The percentage at which your money grows annually. It can be fixed or variable, depending on the investment.

Compounding frequency: How often the interest is added to the principal. This could be daily, monthly, quarterly, or annually.

Time: The duration for which your money is invested. The longer your money is allowed to compound, the more significant the effect.

The more frequently interest compounds, the faster your money grows. For instance, if interest compounds daily rather than yearly, you’ll earn more interest on your initial investment over the same period of time.

That’s why understanding compounding frequency is important when choosing investments like bonds or stocks.

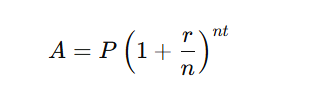

Compound interest formula

The formula for calculating compound interest is: A = P (1+ nr)^nt

Where:

A is the amount of money accumulated after interest (principal + interest)

P is the principal amount (initial investment)

r is the annual interest rate (in decimal form)

n is the number of times interest compounds per year

t is the time (in years) the money is invested for

How to calculate compound interest

While using a compound interest calculator or other financial tools might be more convenient, you can also calculate compound interest manually using the compound interest formula. Let’s break this down further with an example to make it clearer.

Compound interest calculation example

Let’s say you invest $1,000 at an annual interest rate of 5%. You plan to keep the investment for 10 years, with interest compounded annually.

Using the compound interest formula:

P = $1,000

r = 0.05 (5% as a decimal)

n = 1 (compounded annually)

t = 10 years

Now, add these values into the formula:

A = 1000 (1+10.05) 1 * 10

A = 1000 (1.05) 10

A = 1000 * 1.6289

A = 1,628.89

So, after 10 years, your initial $1,000 investment grows to $1,628.89, with $628.89 earned from compound interest.

The power of compounding over time

What makes compound interest so powerful is its ability to generate more significant returns over time. In the example above, the $1,000 initially earned $628.89 in interest over 10 years. But what happens if you leave that money invested for longer periods, say 20 or 30 years?

Let’s see how it works with a 20-year investment period. Using the same 5% interest rate and the original $1,000 investment:

A = 1000 (1+10.05) 1 * 20

A = 1000 (1.05) 20

A = 1000 * 2.6533

A = 2,653.30

As you can see, by doubling the time, your $1,000 investment has grown to $2,653.30. The compound interest you’ve earned over 20 years is $1,653.30—more than double the amount you earned in the first 10 years.

Real-life examples of compound interest

Let’s take a look at a few real-world scenarios where compound interest can be a game-changer for your investments.

Example 1: Retirement accounts (401(k) and IRAs)

One of the most common places people experience the power of compound interest is in retirement accounts like a 401(k) or an IRA. These accounts may often offer tax advantages that allow your investments to grow without immediate tax implications, and they benefit from compound interest.

For instance, let’s say you invest $5,000 per year into your 401(k) account, earning an average annual return of 7%. After 30 years, your account balance may look like this:

Annual contribution: $5,000

Interest rate: 7% annually

Investment period: 30 years

Example 2: Dividend stocks

If you invest in dividend-paying stocks, you can take advantage of compound interest. Companies that pay dividends distribute a portion of their profits to shareholders, typically every quarter. You can reinvest these dividends by buying more shares of stock, which then may generate more dividends.

Let’s say you invest in a stock that pays a 4% annual dividend, and you reinvest your dividends each year. Over time, the number of shares you own may increase, and so does your dividend income. This creates a compounding effect, allowing you to accumulate even more dividends, which you can reinvest again.

If you had $10,000 invested in such a stock, after 10 years with reinvested dividends, you may have a significantly higher balance than if you simply took the dividends as cash.

Example 3: Savings accounts

Although savings accounts typically offer lower interest rates than stocks or bonds, they still benefit from compound interest. If you place $10,000 into a high-yield savings account that offers a 3% annual interest rate, your balance will grow over time.

Let’s say interest is compounded monthly. Using the compound interest formula, your $10,000 grows to about $13,439.13 after 10 years at 3% interest.

This is a good example of how compound interest may help you grow your money over time even in low-risk savings options.

Potential advantages of compound interest

Exponential growth: Compound interest allows your investment to grow at an accelerating rate because interest is calculated on both the principal and the accumulated interest.

Increased earnings with frequent compounding: The more frequently interest compounds (e.g., daily vs. annually), the greater the growth of your investment.

Wealth building over time: Compound interest may help you accumulate wealth over time, especially in long-term investments like retirement accounts.

Low risk: In savings accounts and bonds, compound interest may provide steady growth with minimal risk.

Encourages long-term investing: The longer you invest, the more significant the effect of compound interest, which may make it ideal for long-term goals like retirement.

Limitations of compound interest

Can accumulate quickly for loans: Compound interest can significantly increase the amount owed on loans or credit card balances, leading to higher debt.

Takes time to see major growth: The benefits of compound interest may take years to become noticeable, making it less suitable for short-term investments.

Fluctuating interest rates: For some investments, interest rates can change over time, potentially reducing the benefits of compounding.

Complexity: Understanding compound interest and its calculations can be difficult for beginners, leading to confusion.

Fees may reduce gains: High fees (e.g., on investment accounts or loans) can offset the growth provided by compound interest.

Bottom line

Compound interest is one of the most important concepts in investing. Whether you’re growing your savings or investing in stocks, understanding how compound interest works can help you make better decisions and maximize your investment returns. As you explore compound interest and plan to take the first step towards investing, remember to leverage Public.com. Public is an all-in-one brokerage where you can build a multi-asset portfolio that includes everything from stocks and options to bonds, crypto, and a High-Yield Cash Account.

We designed Public for investors who take their financial futures seriously and seek a transparent platform focused on long-term growth. Join Public today and start building your multi-asset portfolio with the tools, data, and insights you need to make informed investment decisions.

Frequently asked questions

1. How does compound interest compare to CAGR?

Compound interest is interest earned on the principal balance along with its accumulated interest. However, compound annual growth rate (CAGR) is the annual return on an investment that’s determined by calculating the initial balance and any interest accrued over the years.

2. Can compound interest make you rich?

There are many effective strategies for compounding. However, depending on the strategy, compound interest may help you build wealth over time depending on your financial circumstances.

We use cookies and similar technologies as described in our

privacy policy.

You can manage your cookie settings at any time.