A Treasury bill (T-Bill) is a short-term loan, with a maturity period of one year or less, backed by the US Treasury Department. These bills are usually sold in denominations of $1,000, but non-competitive bids may reach up to $5 million. T-bills require a low minimum initial investment and carry a low risk, making them a reliable investment option.

Investors can buy U.S. Treasury bills at auction through both noncompetitive and competitive bidding. They may also choose to purchase T-bills on the secondary market. After purchasing, the investor earns money when the bill reaches the end of its maturity period. Treasury bills have a maturity date of between four weeks and one year.

Treasury bills (T-bills) are short-term investments issued by the US government.

T-bills can be bought in a variety of denominations, with a minimum cost of $100. Investors buy T-bills at a discount and receive the full value when they reach maturity.

The maturity period for T-bills is short and ranges from one day to one year. The most common maturity periods are 4, 8, 13, 17, 26, and 52 weeks.

In order to fund government projects, the U.S. Treasury department sells Treasury securities to investors. One variety of these securities is the Treasury Bill, which stands out because of its short maturity period.

Investors buy Treasury bills, which are backed by the government, at a discount from their face value. Investors can then redeem the T-bills they have purchased after the bill’s maturity period of up to a year.

It is also possible to cash out the bill before it finishes maturing. In this case, the Treasury bill’s owner can resell it through the secondary market.

When investors redeem their Treasury bills at maturity, the federal government then pays them the full face value of the security. Because they have purchased the Treasury bill at a discount from its face value, the difference earned results in investment income, which is fixed at the time of purchase based on the purchase price.

Minimum purchases and denominations

Treasury bills have a low minimum cost of $100, making them a potentially inexpensive and accessible option to add to your investment portfolio. However, the United States government typically issues Treasury bills in denominations of $1,000 or higher—even up to several million dollars.

How can I buy Treasury bills?

One of the easiest ways to buy T-bills is with a Public Treasury Account. Simply move your cash into Public by linking a bank account or making a debit card deposit, make an account, and you’ll be able to lock in a 3.95% return rate*.

In a competitive auction on TreasuryDirect.gov, the US government’s auction site. Bidders set the purchase price of T-bills by putting out offers to buy the bills.

In a non-competitive auction on Treasury Direct. T-bills are sold to bidders at a pre-fixed rate. Treasury bill rates are assigned based on the average purchase price of T-bills in competitive auctions.

In order to purchase a Treasury bill on the secondary market, investors must use a bank or a brokerage licensed to sell T-bills. Some brokerages offer the ability to purchase Treasury bills and it’s easy to do using a Public Treasury Account.

After purchasing the Treasury bill, the new owner will receive documentation verifying that the U.S. Department of the Treasury is accountable for paying them, in accordance with the terms of the bill they have purchased, at the time of the bill’s maturity,

How do you make money on Treasury bills?

Treasury Bills lend money to the government, which is used to fund debt & ongoing expenses such as military equipment & salaries. T-bills are bought at a price lower than their face value, which is typically $100, and redeemed at maturity for the face value. The difference between the purchase price and face value is the interest earned

Did you know?

Any earnings from T-bill investments only become available after the owner cashes out by either waiting until the bill matures or selling it in the secondary market.

Thus, the amount the investor earns from cashing out a T-bill is equivalent to the difference between the bill’s par value and the discount rate at which it was originally purchased.

What is the maximum maturity for Treasury bills?

The maximum security for Treasury bills is one year, or 52 weeks. Even this maximum is short compared to other Treasury securities, making Treasury bills a short-term investment. However, other common increments for the maturity of Treasury bills include 4, 8, 13, 17, and 26 weeks. With a Treasury Account from Public, you can get easy access T-bills with different maturity periods

While T-bills can therefore have maturities significantly shorter than the one-year maximum, a longer maturity period has usually been correlated with a higher interest rate on the bill. Interest rates change daily and investors should always check the current Treasury yield curve to make sure the rate they are receiving for the length of the desired bond is appropriate for their needs.

Benefits of investing in T-bills

Backed by US government – largely safe from market risk

Exempt from state and local taxes

Low minimum investment (as little as $100)

The single biggest advantage of purchasing T-bills is that they are more or less free from market risk.* Because they are backed by the US government, the default risk for these investments is close to zero. Investors are essentially guaranteed to earn back the difference between the investment’s face value and its discounted purchase price if they hold the T-bill to maturity.

When you buy T-bills using Public, you lock in a 3.95% yield rate* — that’s higher than a high-yield savings account**. You’ll have the full faith of the US government backing the bill and SIPC insurance for up to $500,000. And if you need the cash, you can withdraw at any time with no fees.

Furthermore, any income made from these investments is exempt from local taxes and state taxes. However, this income is not exempt from federal taxes. You should consult your legal and/or tax advisors before making any financial decisions.

Finally, because these bills require a low minimum investment—as low as $100—they provide a low-risk and low-price investment opportunity, especially in times of economic turmoil when higher-yield investments entail more risk for the purchaser.

Tend to yield lower returns in periods of high inflation

While T-bills are low-risk, they do carry interest rate risk. Treasury Bills are fixed-income investments. Therefore, when interest rates go up unexpectedly, the value of T-bills decreases. T-bills with longer maturity periods tend to be most sensitive to interest rate risk.

Another limitation of these investments is simply that they tend to yield low returns relative to returns earned on other securities. In other words, anyone considering T-bills as an investment should weigh the advantage of the security’s low risk against the disadvantage of their lower rewards.

Finally, these bills are subject to inflation risk. If the rate of inflation is especially high, investors may find that their real returns are effectively lowered and that the return they receive from their T-bills has not even kept up with inflation. Investors should consider the rate of inflation alongside the return guaranteed on an individual T-bill purchase. If inflation rates are high, people considering buying T-bills should take this into consideration and understand the impact.

How are treasury bills taxed?

Generally speaking, Treasury bill taxes are levied at the investor’s marginal tax rate. Income earned from investments in T-bills is exempt from both state and local taxation, which offers one advantage for taxpayers who invest in these securities, especially for those who live in states where local income taxes are high. However, the income earned from T-bills is still subject to federal income tax.

However, if you buy a discounted T-bill and sell it for a profit, that income may be taxed as a capital gain. You should consult your legal and/or tax advisors before making any financial decisions.

As mentioned above, a variety of external factors can affect the price of T-bills. In addition, the maturity period of a given T-bill can also affect its price.

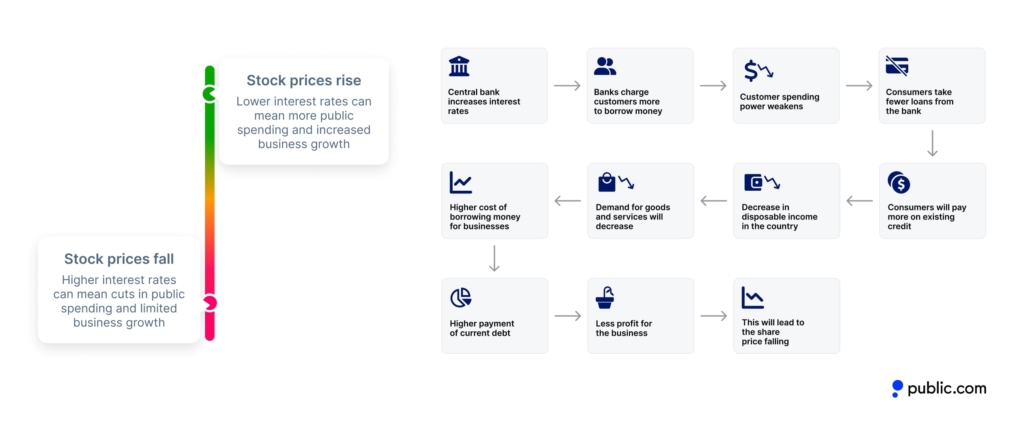

When the economy and stock market are thriving, and investors have a variety of seemingly appealing options, T-bills become less appealing by comparison. After all, one of the main advantages of T-bills is their low risk to investors—but when the risk of losing money is generally thought to be lower, T-bills lose that special advantage and interest rates tend to rise. In this situation, the price of T-bills may drop if rates move higher too quickly.

Meanwhile, the interest rates set by the federal reserve can also have an impact on T-bill prices: when the rate of interest is falling, the value and price of T-bills increases. When interest rates are climbing, their value instead decreases as investors seek out higher-yield options.

Inflation can also affect the price of T-bills. High inflation can lower the real return yields for these investments. This is because they are fixed-rate investments, so the guaranteed return awaiting purchasers at the end of the bill’s maturity may have dropped in value when adjusted for inflation. If inflation is higher than expected during the life of the T-bill, than the real return is lower than the investor may have assumed when he purchased the T-bill – if inflation turns out to be lower than expected, however, the investor may receive a higher real return than assumed.

Finally, while all T-bills are sold at a discount from their face value, those with longer maturities are sold at a greater discount. T-bills with maturities at or near the one-year limit have also historically had higher yields than those with shorter maturities, though interest rates change daily and investors should always check current rates for different maturities of T-bills.

Differences between T-bills, T-notes, and T-bonds

T-bills are short-term securities and have maturities of between a few weeks and a year. T-notes have maturities of between two and ten years with bi-annual interest payments. T-bonds usually mature in 20-30 years, and have historically yielded the highest returns out of these three options.

Conclusion

The Fed’s recent interest rate increases has made investing in T-bills particularly appealing for many investors. T-bills currently yield a return of 3.95% (as of 09/11/2024) and outperform many other low-risk options, including high-yield savings accounts. Treasury Bills have a short maturity period and are backed by the full faith of the US government, making them a strong option for investors in need of a short-term and low-risk investment vehicle. In the current economic climate, T-bills also offer a higher yield return than many other investments.

You can invest in T-bills using Public’s Treasury Account. It’s easy and only takes a few steps to get started.

Can you sell T-bills before it matures?

Yes, you can sell a T-bill before it matures. However, you are subject to the price of the T-bill in the market at that time and are not guaranteed a price or return if you sell prior to maturity.

What taxes do I need to pay on T-bills

You’ll pay federal taxes at your marginal rate on the interest earned, which is calculated as the difference between the price at maturity ($100) and the purchase price of the T-bill. This interest is exempt from state and local taxes, though you should consult your legal and/or tax advisors before making any financial or tax decisions.

Are Treasury Bills a good investment?

Treasury Bills are generally considered very safe investments due to their low risk and backing by the US government. However, they may not return the kind of results expected from the stock market or other higher-risk securities.

When should I invest in Treasury bills vs. bonds?

This decision often relies on the investor’s time horizon and risk tolerance. Short-time horizons tend to be better fitted for T-bills, while longer-time horizons work well with bonds.

We use cookies and similar technologies as described in our

privacy policy.

You can manage your cookie settings at any time.