Bonds are among the most reliable and flexible investment options available. Whether you’re seeking steady income, portfolio diversification, or a less risky alternative to stocks, bonds can meet your needs.

If you’re curious about how bonds work, the types available, and the benefits they offer, this guide will provide the insights you need to make informed investment decisions.

A bond is a type of loan issued by a government, corporation, or other organization to raise funds. When you purchase a bond, you are essentially lending money to the issuer in exchange for regular interest payments, known as the coupon.

These interest payments are typically made at fixed intervals (e.g., annually or semi-annually). Bonds have a specific maturity date, which is when the issuer repays the principal amount of the loan. Once a bond matures, it ceases to exist as the loan is fully repaid.

In simpler terms, bonds work by providing investors with a fixed income through regular interest payments, and at the end of the term, the issuer returns the original loan amount (the principal). Bonds are commonly used as a low-risk investment option and can range from short-term to long-term durations.

For example, if you purchase a bond for $1,000 with an annual interest rate of 5%, you will earn $50 each year until the bond matures. At maturity, the issuer returns the $1,000 principal to you.

What are common bond terms?

Bonds are a popular investment, and as such, a specific set of terms has developed to describe them. While the terminology may seem confusing at first, understanding these terms will make it much easier to grasp important bond-related information and make informed investment decisions.

Bond Term

Description

Coupon

The interest rate the bond pays out, which typically remains fixed once the bond is issued.

Yield

The return you get from the bond, calculated by dividing the bond’s coupon by its changes in value.

Face Value

The bond’s value when issued, also known as its "par" value. The most common face value is $1,000.

Price

The bond’s market price if traded on a secondary market, influenced by the bond’s coupon compared to other similar bonds.

Maturity

The length of time it will take to earn back the bond's face value, with most bonds ceasing to exist once they reach maturity.

Callability

The option for some bonds to be paid off early by the issuer, often with extra compensation for the bondholder.

Put Provisions

An option for certain bonds to be sold back to the issuer before maturity, typically on a specific date.

Convertible Bonds

Bonds that can be converted into a set number of shares of stock in the issuing company or exchanged for cash equivalent.

Secured Bonds

Bonds backed by collateral, where the collateral is distributed among bondholders if the issuer defaults.

Unsecured Bonds

Bonds not backed by any assets, relying on the issuer’s creditworthiness for their value.

What are bond yields?

Bond yields measure the return on investment from holding a bond. Several types of yields may be used depending on the situation:

1. Yield to maturity (YTM):

YTM estimates the return if the bond is held until maturity with interest reinvested. Since interest is paid at various intervals, the actual return may not align exactly with the face value. Calculating YTM can be complex, so it’s best done with spreadsheet software or a financial calculator.

2. Current yield:

The current yield compares the bond’s annual interest payment to its current price. It focuses only on the income generated by the bond, not capital gains or losses, making it useful for assessing immediate income.

3. Nominal yield:

Nominal yield is the annual interest payment divided by the bond’s face value. It’s primarily used in other yield calculations, as it doesn’t account for changes in the bond’s market price.

4. Yield to call (YTC):

For callable bonds, YTC estimates the return if the bond is paid off before maturity. Like YTM, it’s best calculated using financial tools.

5. Realized yield:

Realized yield estimates the return when the bond is sold before maturity. It provides an estimate of the bond’s future price and can be calculated with spreadsheet software or a financial calculator.

These yield types may help investors understand the potential return on their bond investments in various scenarios.

What is the relationship between bonds and interest rates?

Bonds and interest rates share a critical inverse relationship: when interest rates rise, bond prices fall, and when interest rates fall, bond prices rise. This connection is essential for investors to understand, as it impacts the value of their bond holdings.

Example table: How interest rates affect bond prices

Scenario

Interest Rate

Bond Price Movement

Reason

Rates Increase

2% → 3%

Prices Decrease

New bonds offer better yields, reducing demand for older, lower-yield bonds.

Rates Decrease

3% → 2%

Prices Increase

Existing bonds with higher yields become more attractive.

Types of investment bonds

Bonds come in different types, each designed to meet specific investment needs. Here are the most common ones:

1. Government bonds

These bonds are issued by federal governments and are considered some of the safest investments because they are backed by the country’s credit. In the U.S., the most common examples are:

Treasury bonds (T-Bonds): Long-term bonds with maturities of 10 to 30 years.

Treasury notes (T-Notes): Medium-term bonds with maturities of 2 to 10 years.

Treasury bills (T-Bills): Short-term bonds that mature in less than a year.

Government bonds are a good choice for investors looking for stability and a steady income.

2. Municipal bonds (Muni bonds)

Also known as “muni bonds, these are bonds put forth by localities to finance public projects or services. Muni bonds take one of two forms: general obligation or revenue. A general obligation bond is backed by the full fair and credit of the issuer. That means the locality can take whatever measures deemed fit to pay the bondholders on time. This may include taxes, selling assets, and the like.

Revenue bonds, meanwhile, are backed by the income generated by whatever project or service being funded. If, for example, the revenue bond is going toward maintaining a park, then a portion of the cost of admission may be used to pay off the bond. The interest paid out by both bonds is exempt from federal taxes, and if you invest in bonds issued by the state in which you reside, then you don’t have to pay state or local taxes either. The interest on municipal bonds tends to be less than comparable corporate bonds.

3. Corporate bonds

Corporations bonds put out by commercial undertakings such as corporations and LLCs. Corporate bonds offer high yields but are not favored by the tax code. Upwards of 40% to 50% from corporate bonds may end up going toward taxes.

4. Agency bonds

These bonds are issued by government-sponsored organizations like Fannie Mae or Freddie Mac. While they aren’t fully backed by the federal government, they are still considered relatively safe investments.

5. Treasury inflation-protected bonds (TIPS)

Treasury Inflation-Protected Securities (TIPS) are designed to protect your investment from inflation. Their principal value adjusts with inflation, so your money keeps its purchasing power over time.

What are the benefits of investing in bonds?

Investing in bonds can offer stability and a predictable income stream, making them an appealing option for many investors. They may also serve as a valuable addition to a diversified portfolio by balancing risks associated with other investments like stocks.

Steady income: Bonds may provide regular interest payments, offering a consistent income stream.

Capital preservation: High-quality bonds can help preserve your initial investment.

Portfolio diversification: Adding bonds to your portfolio may reduce overall risk and balance market fluctuations.

Lower risk: Bonds with higher credit ratings can be less risky compared to other investments.

Tax advantages: Some bonds, such as municipal bonds, may offer tax-free interest income.

Predictable returns: Fixed-rate bonds can provide predictable returns over a set period.

Bonds are generally safe investments, but they do come with some drawbacks:

Credit risk: The risk that the issuer may not meet the terms of the bond. Higher-rated bonds are safer but offer lower returns, while lower-rated bonds (junk bonds) carry higher risk but can offer better returns.

Liquidity risk: Bonds are less liquid than many other investments, meaning they might be harder to sell without losing value.

Reinvestment risk: The risk that interest rates might drop by the time your bond matures, potentially reducing the return on reinvested funds.

Understanding these risks helps you make informed decisions when investing in bonds.

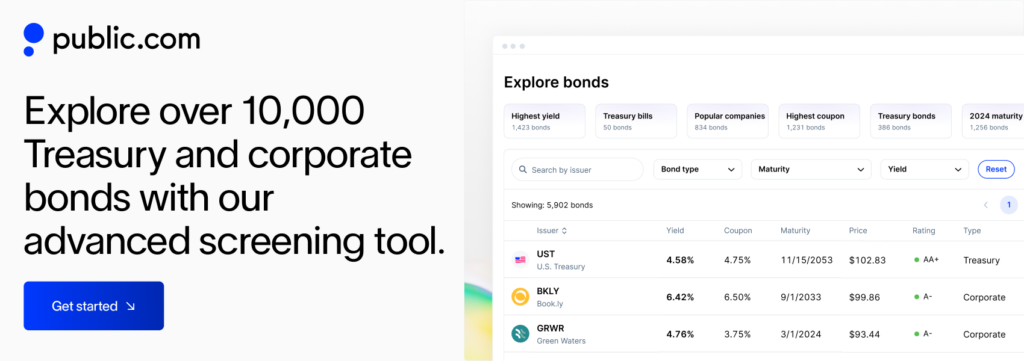

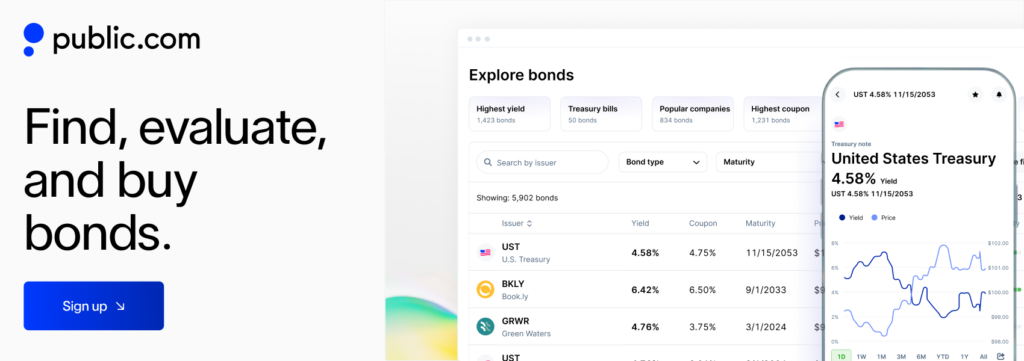

How to invest in bonds on Public.com?

Know the simple 4 steps to invest in bonds using the Public app.

1. Sign up for a brokerage account on Public

You can sign up for an account on our website or download the Public app from the App Store (iOS) or Google Play Store (Android).

2. Add funds to your Public account

There are multiple ways to fund your Public account – from linking a bank account to making a deposit with a debit card or wire transfer.

3. Choose how much you’d like to invest in bonds

Navigate to the xxplore page. Then, search for the bond of your choice in the search bar. When you see the bond appear in the results, tap it to open up the purchase screen.

4. Manage your investments in one place

You can find your newly purchased bond in your portfolio – alongside the rest of your stocks, options, crypto, ETFs, and Treasuries.

Bottom line

Bonds can play a key role in building a diversified portfolio, offering opportunities for income and stability. With Public, investors can track bonds alongside stocks, options, crypto, ETFs, and Treasuries within a single account.

Public also offers AI Agents, which allow investors to automate investing workflows based on their portfolio goals and strategies. Investors define the instructions while remaining in control of investment decisions.

If you’re interested in investing in bonds, you can open a brokerage account on Public and explore available fixed-income investments alongside other asset classes.

We use cookies and similar technologies as described in our

privacy policy.

You can manage your cookie settings at any time.