Navigating the world of trading options? The Options Greeks might sound like an ancient topic, but they’re crucial navigators in this financial odyssey. Let’s unravel their mystique together.

The Greeks in Options Trading: Delta, Gamma, Theta, Vega, and Rho Explained

Table of Contents

Understanding Options Greeks

Options Greeks are mathematical tools that represent the sensitivity of an option’s price to various factors like the underlying security, volatility, time decay, and interest rates. Each Greek corresponds to a different factor and provides option buyers and option sellers with a lens to gauge how potential changes can impact an option’s price.

In the options market, the Greeks act like a roadmap. They help traders navigate the complexities of risk and reward. By understanding these Greeks, traders can anticipate how an option’s strike price will change in different scenarios. This insight is crucial for making smarter choices in strategy selection and risk management.

For instance, if you know how much an option’s price will change with a $1 move in the underlying security (thanks to Positive Delta), or understand how much an option’s value will drop over time (thanks to Theta), you’re better equipped to make informed decisions. Each Greek plays a unique part, and mastering them equips a trader with a comprehensive toolkit for the market’s ever-changing dynamics.

Use of the Greeks

Options trading, at its core, is about gauging and managing risks. The Greeks play an instrumental role in this by offering insights into how various factors can influence an option’s price. When option buyers and sellers aim to optimize their strategies or manage risk in their portfolios, they often turn to the Greeks for supporting indications.

The Black-Scholes model uses the Options Greeks to offer insights into how options are priced. This model helps in calculating the estimated value of an option contract, taking into account time and various risk factors. Derivative traders use the Black-Scholes model as one of several methods to estimate the pricing of option contracts.

Incorporating the Greeks into this model helps traders to get a nuanced understanding of the factors influencing an option’s price. This assists them in aiming to strategize more effectively and make decisions that consider both market dynamics and their individual investment objectives, bearing in mind the inherent risks and uncertainties.

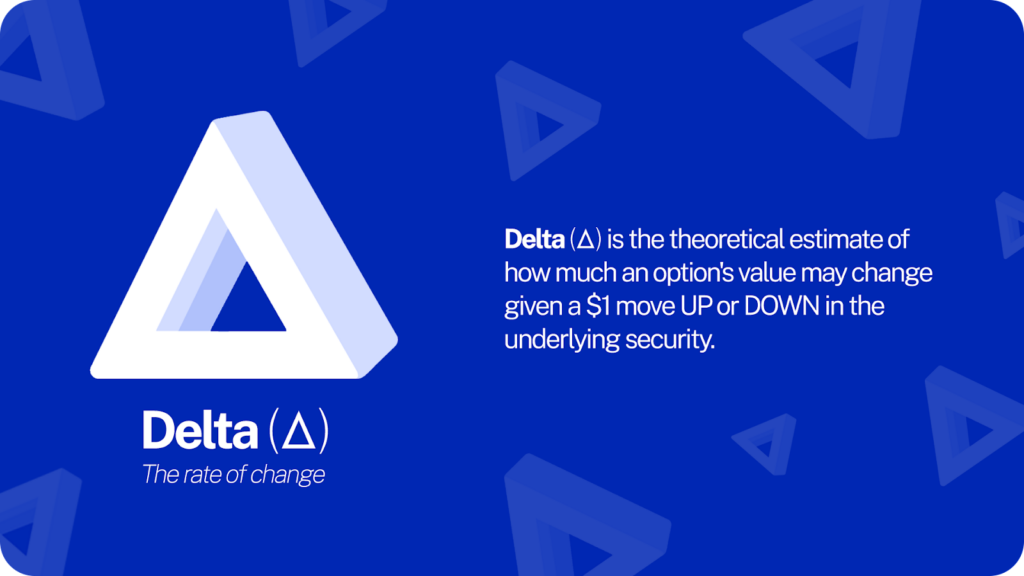

Delta: The Rate of Change

Delta, often denoted as the first derivative of the option’s price concerning the underlying security’s price, is one of the most essential Greeks in trading options. It represents how much an option’s price will adjust given a $1 change in the underlying asset, be it a stock or other financial instrument.

The primary essence of Delta lies in its depiction of sensitivity. It answers the question: “If the stock price changes by a certain amount, how much can I expect the option’s price to move?”

Typically, for every option, the value of Delta will fall between 0 and 1 for call options and -1 to 0 for put options. A call option with a Delta of 0.50, for instance, indicates an option’s price will rise by $0.50 for a $1 increase in the stock price. Conversely, a put option with a Delta of -0.50 indicates the option’s price will decrease by $0.50 for a $1 rise in the stock price.

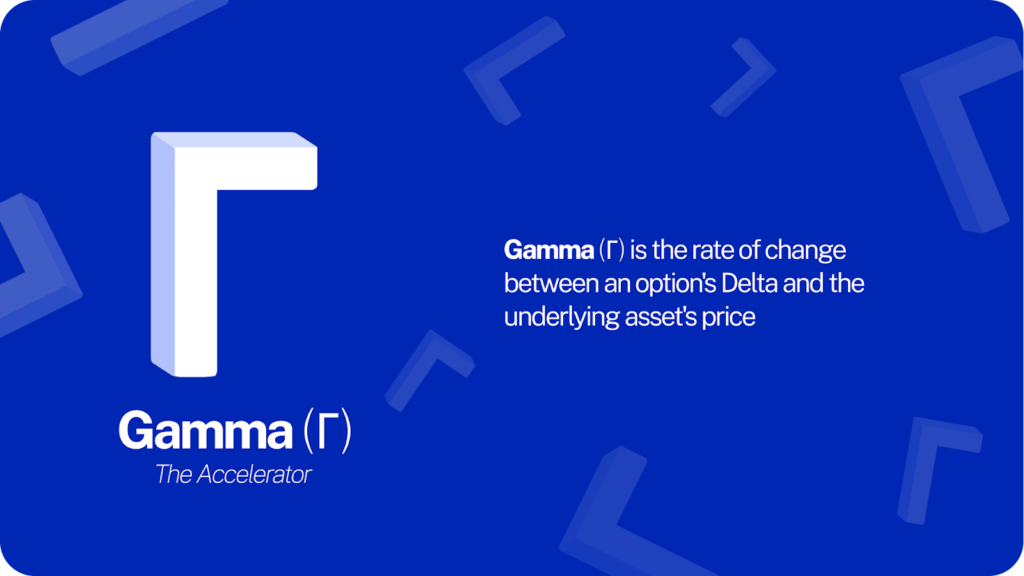

Gamma: The Accelerator

While Delta gives us a snapshot of how the price of an option might change with a $1 move in the underlying security, Gamma provides a deeper layer of insight. Often termed the ‘accelerator’, Gamma is the rate at which Delta changes for every $1 movement in the stock. In other words, if Delta tells us the speed at which option prices change, Gamma tells us how much that speed is accelerating or decelerating.

Every option will have a Gamma value associated with it, which represents the change in Delta for a unit change in the stock price. It’s important to note that Gamma is at its highest for at-the-money options and progressively reduces as options move in-the-money or out-of-the-money.

To illustrate in simpler terms, one could compare these concepts to driving a car. Consider a car’s speedometer. Delta might be the speed at which you’re driving, say 60 mph. If you accelerate or decelerate, the rate at which your speed changes, be it going from 60 mph to 65 mph or down to 55 mph, can be likened to Gamma.

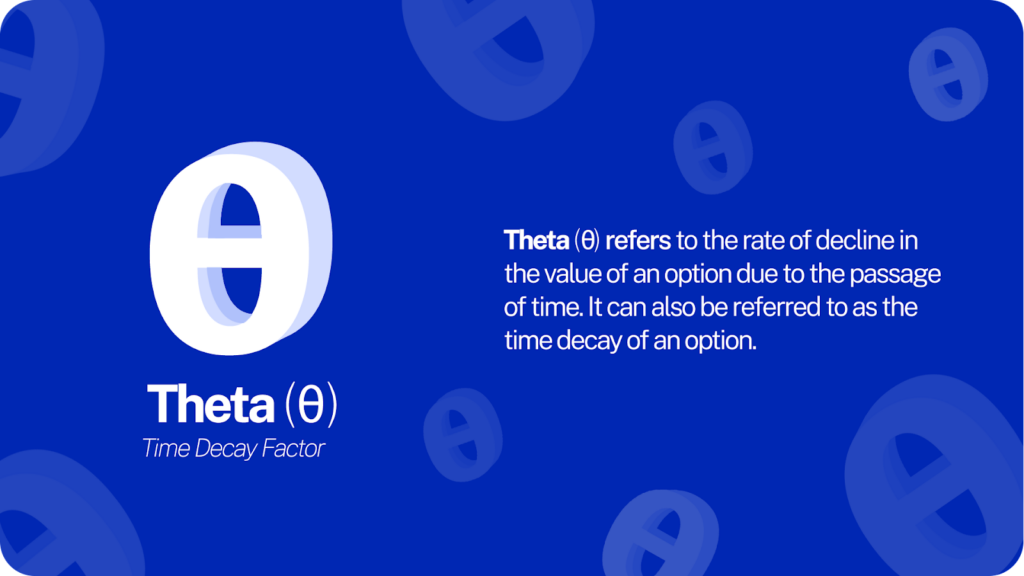

Theta: Time Decay Factor

Theta, commonly referred to as ‘time decay’, indicates the diminishing value of an option as it approaches its expiration date. With all else being equal, an option will lose some of its value with each passing day due to Theta.

Let’s say you buy a ticket to a concert. As the event day nears and if you haven’t used the ticket, its value may decrease, especially on the day right before the concert. Similarly, in the world of options trading, the closer the option gets to its expiration date, the less time there will be for the stock to make a significant move. This decrease in potential profitability is reflected in the option’s price through the concept of Theta or time decay.

Every option has a Theta value that signifies how much the option’s price will decrease daily due to time decay. For instance, an option with a Theta of -0.05 will lose 5 cents per day as long as all other factors remain constant. It means that as each day passes, the option becomes less valuable by that Theta amount.

Vega: Sensitivity to Volatility

Vega is a metric representing the sensitivity of an option’s price to changes in market volatility. Unlike most other Greeks which have clear ties to factors like stock price, time decay, or interest rates, Vega focuses solely on the unpredictability of market movements.

Volatility is a measure of the unpredictability or variability of an asset’s price over time. Options on stocks or assets with high volatility typically command higher premiums because of the greater potential for significant price swings, which can translate to higher profits (or losses).

Every option has a Vega value that indicates how much an option’s price will change for a 1% change in implied volatility. For instance, if an option has a Vega of 0.12, it means that for every 1% increase in implied volatility, the option’s price will rise by 12 cents (and vice versa for a 1% decrease the options price will decrease by 12%).

Rho: The Interest Rate Sensitivity

Rho might not be as frequently discussed as the likes of Delta or Theta in options trading, but it carries great significance for those monitoring macroeconomic indicators. Rho reflects the relationship between an option’s price and the prevailing interest rates, particularly the risk-free rate.

Rho quantifies how much an option’s price is likely to change for every one-percentage-point alteration in interest rates. If you have a call option priced at $4 with a Rho of 0.25, it means that if interest rates were to rise by 1% (say, from 3% to 4%), the price of that call option would increase to $4.25. Conversely, if interest rates were to decline by 1%, the value of the call option would drop to $3.75.

Implied Volatility

Although not strictly a member of the Greek family, implied volatility plays a pivotal role in the world of options trading. It represents a theoretical prediction of a stock’s potential volatility in the future based on current market conditions. It does not provide any guarantees about future stock movements or volatility.

Implied volatility gauges the market’s sentiment regarding the future volatility of an underlying stock. This assessment goes beyond merely analyzing the stock’s historical volatility; it also factors in external influences like upcoming earnings announcements, prevalent market rumors, and anticipated product launches.

Minor Greeks: Diving Deeper

Beyond the Greeks discussed above, there exists a set of lesser-known yet significant metrics: the minor Greeks. Though not always at the forefront of trading discussions, these metrics offer added layers of depth and understanding of the intricacies of option pricing and sensitivity.

Let’s delve into some of the minor Greeks:

-

Lambda: This metric gauges the sensitivity of a stock’s price to a 1% change in implied volatility.

-

Epsilon: Focused on dividends, Epsilon measures the sensitivity of an option’s value to variations in the dividend yield of the underlying stock.

-

Vomma: A second-order Greek, Vomma indicates how Vega’s sensitivity fluctuates with changes in volatility.

-

Vera: This Greek provides insights into Rho’s sensitivity concerning volatility shifts.

-

Speed: As the name suggests, Speed measures the rate at which Gamma reacts to price shifts in the underlying stock.

-

Zomma: This metric delves into how Gamma’s sensitivity changes with volatility fluctuations.

-

Color: With a focus on time, Color measures Gamma’s sensitivity as time passes.

-

Ultima: Delving deeper into volatility’s layers, Ultima assesses Vomma’s sensitivity to volatility changes.

While the primary Greeks are used by many traders, understanding these minor Greeks can offer advanced insights, especially for those looking to refine their strategies and deepen their grasp on the multifaceted world of options trading. Given the complexity and advanced nature of these concepts, they’re often leveraged by traders with extensive experience in the field.

Mastering the Greeks: A Path to Informed Options Trading

For options traders, the Greeks ensure they are equipped with the knowledge to make strategic moves with minimal risks and maximum potential returns. However, it is important to recognize that all trading involves risks and there are no guarantees of return.

In your pursuit of mastering options trading, it’s invaluable to partner with a platform that prioritizes your interests and offers unparalleled support. That’s where Public.com comes into play.

Explore a multitude of investment avenues with us. Benefit from real-time market data, customized reporting, and valuable insights from industry experts. Our platform is fully regulated, ensuring transparency and asset protection in line with industry standards.

Start your informed investment journey today!